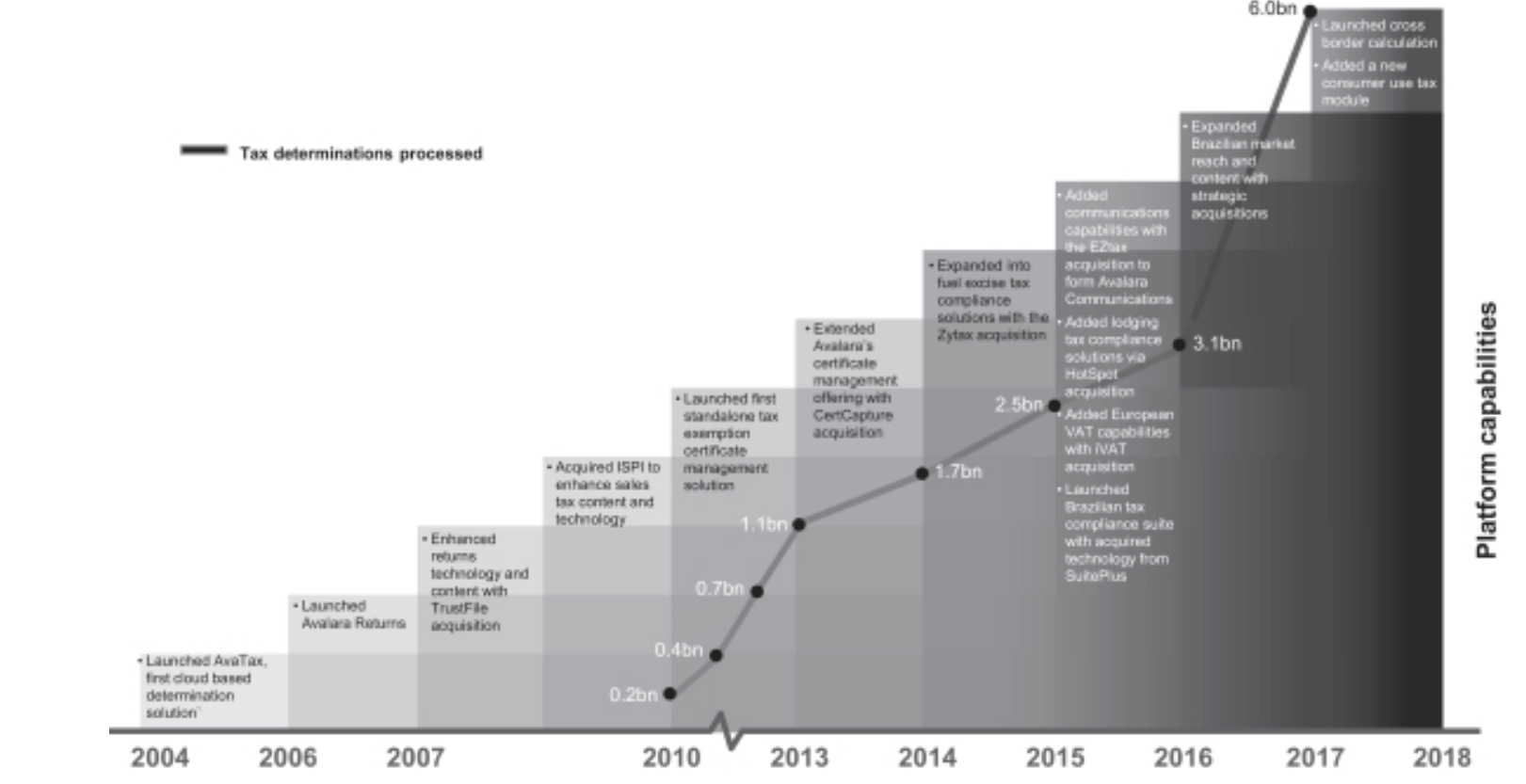

Avalara helps its customers by providing a platform that automates tax compliance. The company is growing rapidly. In 2015 it had sales of $113m. As you can see from the table below that is expected to reach $728m by calendar 2022. The number of core customers (who accounted for 85pc of total revenue in 2017) has increased from 6,250 in 2016 to 13,300 for Q2 2020. Each customer is spending more as the group rapidly increases its number of products. CEO, Scott Mcfarlane, said at the June 2020 analysts’ day that Avalara was becoming a ‘product machine’.

The addressable market is huge. In the prospectus they talk about an $8bn opportunity in the US alone. Additional products come on top of that and the group has global ambitions. The group vision is “to be part of every transaction in the world”.

One highly rated US analyst said, not long ago, that if he could only hold one share he would choose Avalara.

The group believes there are four powerful tail winds driving growth – the acceleration of e-commerce adoption, acceleration of the move to the cloud, growing emphasis on return on investment and efficiency and increased regulation as governments try to boost their tax take.

I see Avalara as a company with the potential to become very large indeed. The share price moved up recently following the $377m acquisition of TTR (Transaction Tax Resources) which comes with 1400 customers including 30pc of the Fortune 500 and 130 employees.

Avalara is an acquisitive company and recently said they had a strong pipeline of targets.

They take an awkward job (tax compliance) off the table and make sure it is done properly. I am not surprised they are growing so fast and see such a huge opportunity.

The chart above gives a flavour of how the company was growing up to the flotation in June 2018. The table below shows how that growth is expected to continue. Like other businesses in the enterprise software space, which is probably my favourite sector, the growth sees the impact of Covid-19 as a growth driver.

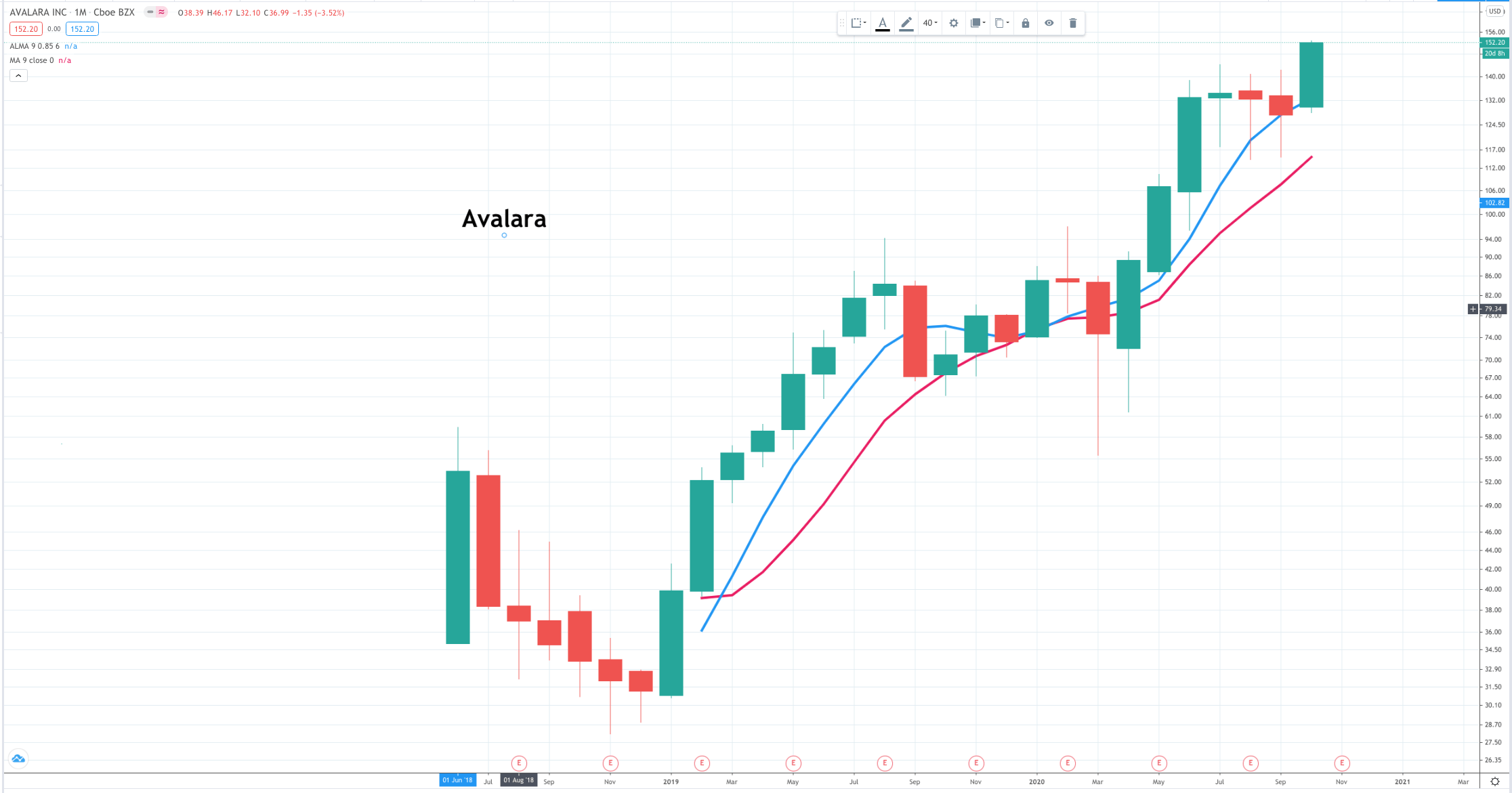

Te chart below, of the share price, ticks the other box for 3G (great growth, great story, great chart).

Avalara/ AVLR Buy @ $152 MV: $12.7bn Next figures: 5 November No of times recommended: 8 Price when first recommended: $50.50

“Avalara’s motto is “Tax compliance done right.” The rise of digital commerce and international trade, coupled with constantly shifting taxation and reporting obligations imposed by the global patchwork of local, regional, state, and national taxing authorities, has created a tremendously complex and onerous compliance burden for businesses of all sizes. Avalara’s mission is to provide solutions for this challenge, allowing companies to focus on their core operations. We provide a leading suite of cloud-based solutions designed to improve accuracy and efficiency by automating the processes of determining taxability, identifying applicable tax rates, determining and collecting taxes, preparing and filing returns, remitting taxes, maintaining tax records, and managing compliance documents. In 2017, we processed an average of over 16m tax determinations per day. Our vision is to be part of every transaction in the world.”

“We believe that the total addressable market for transaction tax compliance solutions is large and underpenetrated. We estimate that the addressable market in the United States alone for the solutions we offer today is over $8bn.”

“We believe this $8bn figure understates our total addressable market, as it does not account for businesses outside the United States, or potential future expansion in the solutions we offer and corresponding potential increases in average annual revenue per customer.”

“While most of our revenue is currently generated from customers located in the United States, we support transaction tax compliance in Europe, South America, and Asia and believe we have a significant growth opportunity in these markets. For example, the OECD estimates that over $1.2 trillion of VAT was collected in Europe for 2016. Although we are in the early stages of developing our international presence and therefore have less historical data with which to assess the size of our market opportunities, we believe that Europe and other jurisdictions throughout the world represent a significant additional addressable market for our transaction tax compliance solutions.”

Like so many companies in the enterprise software space (software developed by one enterprise to help other enterprises run their businesses – a key part of digital transformation) it is not easy to get your head around exactly what Avalara does and, being about tax, it is extremely boring. They do a job that nobody else wants to do.

Fortunately for the group’s shareholders and customers Avalara’s founders don’t feel the same.

“Cofounders Rory Rawlins, Jared Vogt, and Scott McFarlane created an entirely new perspective for processing sales tax. “Sales tax is boring, but the business of sales tax is really, really exciting,” said Scott, CEO of Avalara. Their passion for the business is apparent and well defined.”

This was in a Forbes article about Mcfarlane at the time of the IPO. I also watched a TV interview with Mcfarlane where he said:

“In a digital world the concept of doing sales tax manually is absurd. It will be automated. It is just a question of when.”

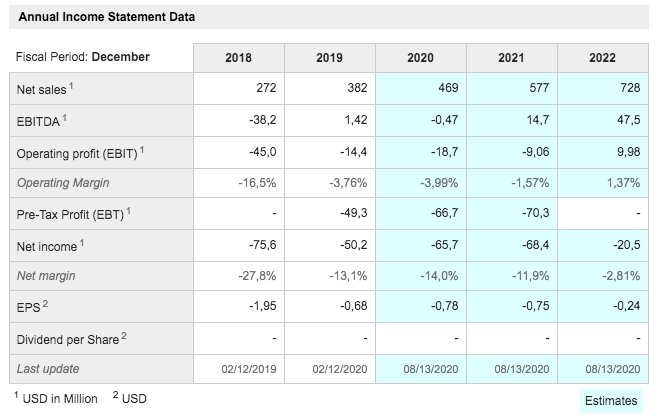

Like many enterprise software companies even though it was founded in 2004 Avalara still makes losses and our table below sees this continuing into 2022. The reason for this is the battle for territory. Most enterprise software companies have huge gross margins and Avalara is no exception. In 2019 on sales of $382m the company made a gross profit of $267m.

The reason why it still reported a net loss is because of massive operating costs, especially on research and development (remember what Mcfarlane said about Avalara being a product machine) and on sales and marketing – the battle for territory.

In 2019 Avalara spent $82.4m on r&d and a staggering $169m on sales and marketing, which would have been $188m but for a new US accounting standard. Companies like Avalara need to spend on r&d and s&m or they die but it is also a way of investing in future growth. When you realise that Avalara is spending $251m a year (65.7pc of revenue) on driving growth you start to see why the business is growing so fast.

They are chasing an incredible prize – they really do want to be part of every transaction in the world and in a cross-border world everybody needs help from them or somebody like them. If they can become the market leader in this space what are they going to be worth. I have no idea but a lot – much more than their current valuation, which is almost tiddler level by US standards.

Also exciting for investors are signs that growth is accelerating.

“Our revenue [in Q2 2020] was $116.5m, up 28pc year-over-year. I was pleased to see our momentum accelerate throughout the quarter, with June representing our best non-December total bookings month ever.”

This growing momentum is happening across the business.

“We are building a global cloud compliance platform company and are backing this effort with a product portfolio that is rapidly growing and a product development cadence that is accelerating.”

Companies like Avalara get into virtuous circles of growth. The more they grow the more they can spend on growth, the more important they become to their customers and so the more they grow. They really are kind of perpetual motion machines which is why investors find them so exciting as investments.

But they are also scary because the losses seem to go on for ever and the climbing share prices lead to wild bouts of profit taking. When Covid struck the shares fell in two months from $97 to $55 before investors realised that ultimately lockdown would benefit companies like Avalara. The ride will be bumpy but all the evidence to date suggests that it will also be extremely rewarding. The shares have almost quintupled from the first day dealings price at the June 2018 IPO.

The group is also helped by its many partners who create a barrier to entry for would-be competitors.

” Avalara has been a partner-centric company since our founding, and our partner strategy has created a competitive moat that also drives growth. The result of this long-term strategy is that Avalara offers far more prebuilt integrations into applications which companies use to run their business than any competitor.

In today’s omnichannel world, this creates a significant differentiator for us. The strength of our offering and long-standing partner relationships play nicely to our advantage when working with prospects using the largest traditional business systems. But our advantage is even greater in the long tail, the hundreds of smaller or specialised applications where we are one of the few automation providers within integration. Each quarter, we add new partners and new integrations to our moat, and we will continue to do so as we drive toward our vision of becoming the global cloud compliance platform. This combination of breadth and depth is incredibly difficult to replicate and represents a key strategic differentiator as we acquire new customers and grow with our existing customers.”

Remember how Datadog describes itself as “the monitoring and analytics platform for developers” (‘the’ not ‘a’) well, Avalara wants to be “the global cloud compliance platform”.

I love it when I see companies both walking the talk with their performance and making it clear that they have huge ambitions. Avalara is another classic example and a worthy member of the QV roster of superstocks.

The group also took the opportunity to raise $575m before expenses by an equity issue. This is around double what it raised in the 2018 IPO and highlights the ability of highly rated businesses like Avalara to fund growth cheaply with relatively minimal dilution of existing investors. The group floated at $24 a share but priced its latest offering at $127.

One of the factors that make software platform stocks like Avalara such exciting investments is a phenomenon known as scaleability. One of the all-time great examples is Google. Two guys created a search algorithm (I think it is an algorithm; it is certainly software based) and have parlayed that into one of the world’s largest businesses.

Old school investments like manufacturers and bricks and mortar retailers could never match that growth because in order to grow they had to keep building factories or opening more stores. Their growth created ongoing costs.

If software companies like Avalara just stop growing profits explode. Indeed margins did rise in Q2 because they slowed investment spending because of the virus. Now they say margins will fall again because they are going to step up hiring, investing, marketing and generally spend more on scaling the business.

Investors are aware of this which is why they value these businesses so highly. They know that slowly but surely as these businesses mature, assuming they win the all-important battle for territory, that operating costs (r&d, s&m and g&a – general and administrative) will start to grow more slowly than sales and profits will climb, probably very rapidly.

In 2009, at the height of the financial crisis, a super fast growing cloud software company, Salesforce.com, briefly stopped investing in growth and stunned investors by reporting a handsome profit. As confidence returned they resumed investing and reverted to their normal pattern of making losses.

This is why, within reason, it is a good sign when a software company is making losses. It means they have a huge opportunity and are investing at scale to take advantage.

The icing on the cake is the network effect which mean there is a marked tendency in the software world for the fastest grower to reach a winner-takes-all position. This is exactly what many of the businesses I feature in QV for Shares are trying to do and what makes them so exciting. The biggest companies in a sector or market niche almost by definition have the lowest costs and become the most profitable.

It is more complicated than that because there is an energy and sense of purpose about newcomers, disruptors, which makes it hard for old-tech incumbents to fight back. The world car industry is on red alert to stop Tesla taking a huge chunk of the global car market but even so looks vulnerable because all the existing big players have to deal with a fossil fuel legacy and a mindset determined by that legacy. Tesla has achieved critical mass while having none of that, which is what makes it so exciting as an investment.

The US stock market is full of investments, which offer similar excitement. It is an amazing time to be an investor – a time to be bold.