AfterPay Limited/ APT Buy now, pay later services Buy @ A$54.52 (Note: US$1= A$1.47; £1 = A$1.82)

Afterpay Limited has transformed the way people pay by allowing shoppers to receive products immediately and pay in four simple instalments over a short period of time. The service is completely free for customers who pay on time – helping consumers spend money responsibly without incurring interest, fees or revolving and extended debt. Afterpay is offered by more than 48,400 of the world’s best retailers and is used by more than 8.4m active customers globally. Afterpay is currently available in Australia, New Zealand, the United States and the United Kingdom where it is called Clearpay. Afterpay is on a mission to be the world’s most loved way to pay.

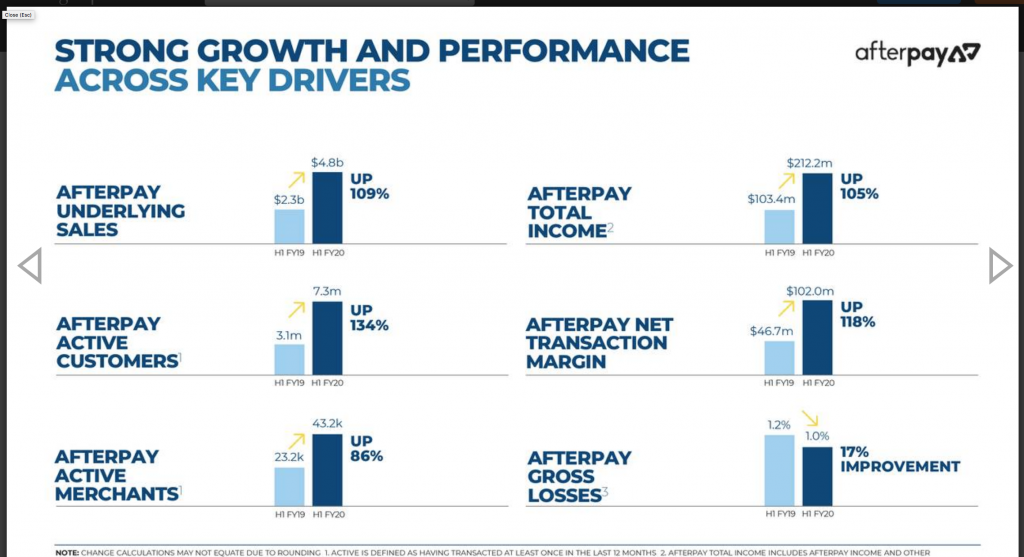

The company reported its half year results on 26 February showing strong growth.

“I’m very pleased to report another strong period of growth across our key performance metrics. Underlying sales and active customers more than doubled in the period-on-period results. Merchants are up 86pc, and total income and net transaction margin are up 105pc and 118pc, respectively. As importantly, we materially improved loss performance while growing our top line over 100pc period-on-period, and we’ll talk a little bit more about that.

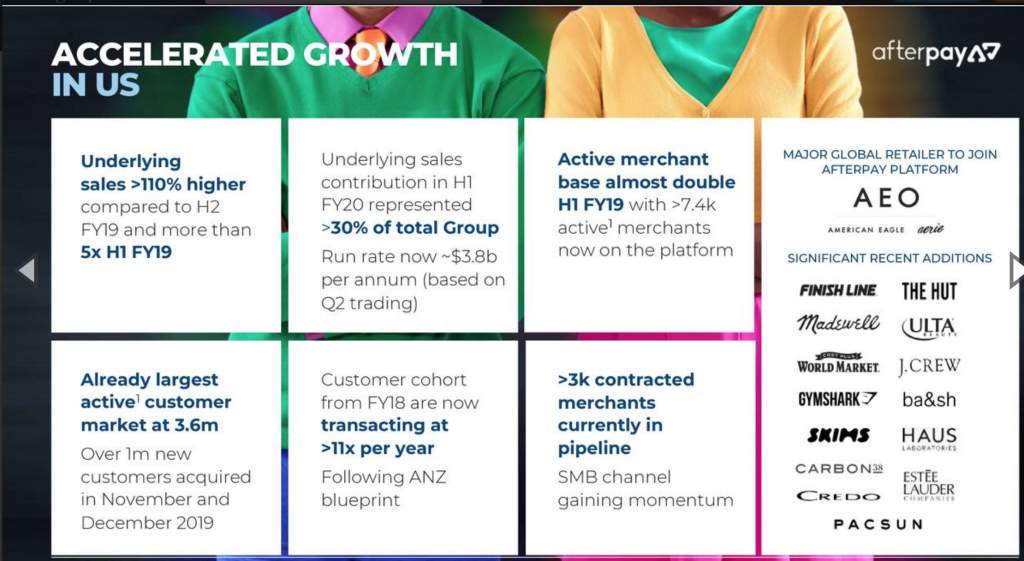

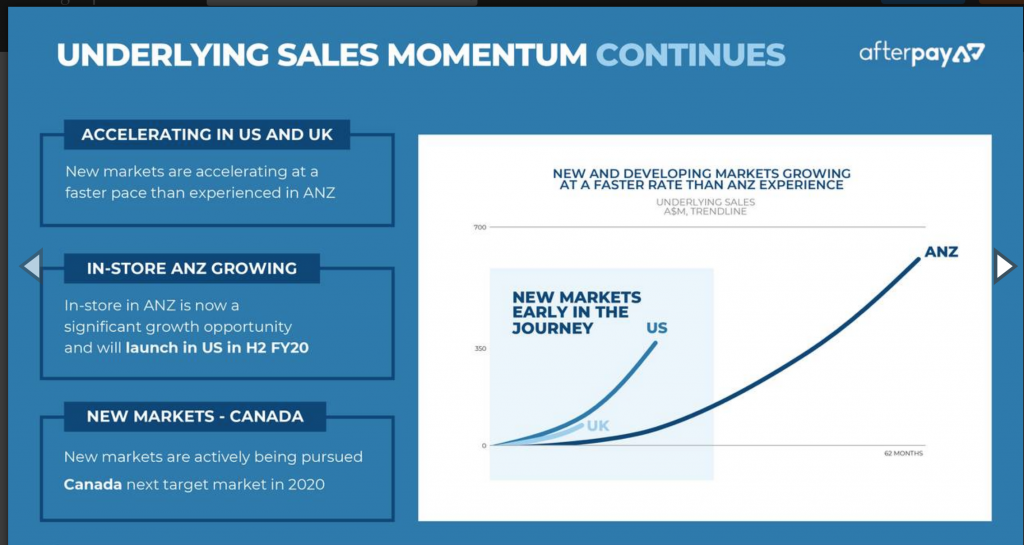

Global underlying sales run rate for Afterpay now is over $11bn based on recent performance. Our global expansion is accelerating, particularly underpinned by the U.S. where underlying sales are now 5x higher than the same time last year. Momentum with market penetration, but also with the Afterpay merchants, whose brands are recognised globally, gives us the confidence and the momentum to continue expanding into new markets, and I’m very pleased to announce that Canada will be launched in this calendar year.

Active customers continue to grow, averaging more than 16,800 per day, which increased to nearly 23,000 new customers per day in November and December. Our active merchants continue to grow, both with very large key brands but also in terms of our small to medium business and midsized business rollout strategy, which continues to climb in all of our markets.

Nick [Mornay, co-founder and chief revenue officer] will talk in a little while about our in-store growth in Australia and New Zealand because it’s been very significant for us, it’s an important differentiator, and we still see there’s a very big growth opportunity in Australia but also globally as we plan to launch in-store in the U.S. in the coming months.

it’s important to remember why we’re different, and in a lot of ways, why we created Afterpay in the first place. Our business model is different because it’s aligned to treating customers well. Simply put, we don’t seek to charge the customer or allow them to revolve in debt. This is different to traditional finance companies, and it’s different to other companies that use the buy now, pay later banner. This is a really important feature because it links to what is, in our view, a very low-risk business model in comparison.

We have the shortest duration book because we don’t allow customers to revolve in debt and we don’t extend the payment terms. As well as maintaining good margins, we’re able to generate high returns on capital employed under this model while still providing what we believe is the most responsible service to customers who want a budget to purchase as opposed to get further into debt.”

We’re delivering sustained growth in a maturing Australia and New Zealand market. And obviously, exponential growth in the newer markets of the U.S. and the U.K.”

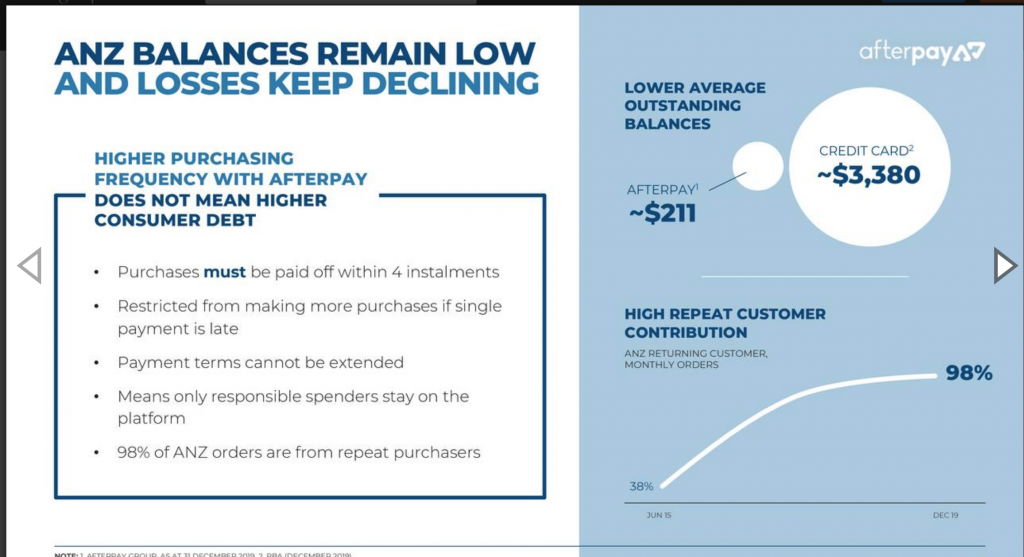

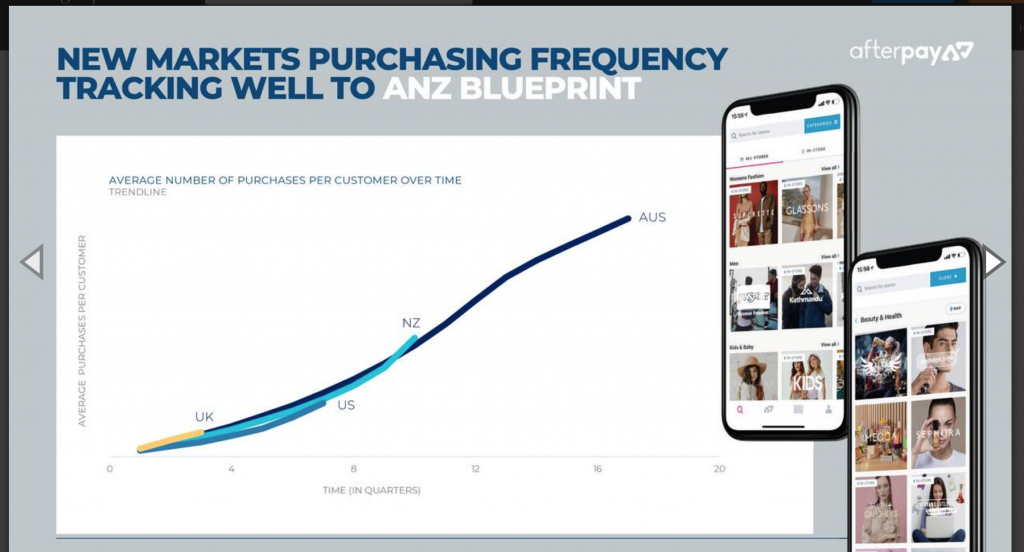

“The ANZ market is delivering really strong growth off of a large base and, to me, is really the blueprint for new regions and why we feel so confident to invest into the curve. So high acceptance rates that we’ve been able to achieve, coupled with really high-frequency rates from not just our older customer demographics but the more recent customer demographics following the same trend really illustrates the strong growth of the market.

We have made a very conscious effort to push in-store, which represents a significantly greater opportunity than the online market just given that the share of online relative to off-line still remains low. And from a new vertical perspective, the ability to scale beyond fashion and beauty into health platforms, travel and other markets represents a really significant opportunity for us.

The fact that our older demographic — our older cohorts are now purchasing almost twice a month or 23x per year really represents their love for our brand and how they continue to use Afterpay frequently as our platform grows into new verticals and expands off-line.

Our platforms are getting far more mature and more sophisticated. And our repeat purchase profile in Australia, now sitting at 98pc, is really important because a consumer can only use Afterpay in the event where their account is not late. So naturally, over time, as you get more repeat customers, we are getting a better profile of consumer who has a better repayment profile because they can only shop in high-frequency levels while still maintaining low outstanding balance levels when their accounts are in good order.”

So to be able to achieve more than $700m of transactions through our off-line channel has been an amazing achievement by the team and in partnership with some of the best retail partners in the world and in Australia. The off-line market is a significant opportunity. So $140bn as compared to online is significantly greater. So as we look to scale our network off-line, as our customers online start shopping offline and our ability to attract new consumers through the off-line channel represents a significant opportunity for Afterpay in Australia and, as Anthony alluded to before, soon to come in the U.S. in the coming months.

The U.K. processed more than $200m of transactions in the first 6 months of trade in H1 FY ’20. So that was from a standing start. We went into the region with no presence. But the ability to leverage our global retail partnerships to launch with ASOS, Boohoo, Marks & Spencer, JD Sports, all businesses that we did have existing relationships with in other regions, really gives us comfort to expand into regions like Canada and more broadly in the future.”

Afterpay’s business may sound simple but sophisticated technology is needed to make this work. So much so that AfterPay is classified as a fintech company.

“The mobile and digital transformation behind Afterpay’s rapid international rise

Afterpay, is one of the relatively few tech success stories this country (Australia) has produced. And it’s through a consistently stable yet increasingly diverse approach to mobile and web capability that the business is capitalising on growing international consumer demand. Four years ago, Afterpay founder, Nick Molnar, debuted an alternative way of providing payment solutions to millennials adverse to credit cards. Since then, the ASX-listed company has been on a fast track to fast-growth, reaching a market cap of greater than $4bn last year. With that has come rapid customer base growth, locally and internationally, as well as in the number of retailers offering the payment service. This is most clearly demonstrated through Afterpay’s digital channels and engagement on its mobile app and web platform. Today, the company boasts of 3.5m monthly active users online, 2.8m mobile app downloads and 1.7m monthly active mobile customers. It also has more than 500m weekly requests via its website and generates 1.3m in-store purchasing codes every month. “There is a lot of humbleness about the rapid growth of Afterpay. We have been very fortunate to have an exciting high-growth opportunity not only as an Australian startup but also as a global one,” Afterpay chief product officer, Kareem Al-Bassam, told CMO. Realising this requires scalable and flexible digital capability. Such progression has been achieved profitably and with current digital presence uptime of 99.999pc thanks, in part, to an ongoing partnership with Dovetail. First brought on two years ago to build Afterpay’s inaugural mobile app, the digital agency has become a key partner in what is a rapidly evolving quest to satisfy international demand for a new way of conducting retail trade. Dovetail looks after the design, development and infrastructure of Afterpay’s web and mobile platforms. The Australian-owned company was established four years ago by co-founders and managing partners, Ash Fogelberg and Nick Frandsen, who originally worked together at New Zealand-based ticketing and events company, 1-Night. Initially, Dovetail was tasked with building Afterpay’s first-ever mobile app. “We had to make big decisions about where we spread existing resources and the team, and place big bets,” Al-Bassam said.

“We had choice to work around how to approach mobile as a company; the demographics we serve, and what would be a competitive differentiator. There were also questions on whether we built it ourselves versus using a partner.” Fogelberg said the first piece was defining and building an app for both IOS and Android devices. It took 90 days to release the first MVP (minimum viable product). “We didn’t know at that stage it would become as big as it has become,” Fogelberg said. “Just off the soft launch, people started talking about the Afterpay mobile app on Facebook, and it shot to number one in the app store.” From there, Afterpay quickly added an in-store payments product, allowing retailers to accept phone-based payments in physical stores.

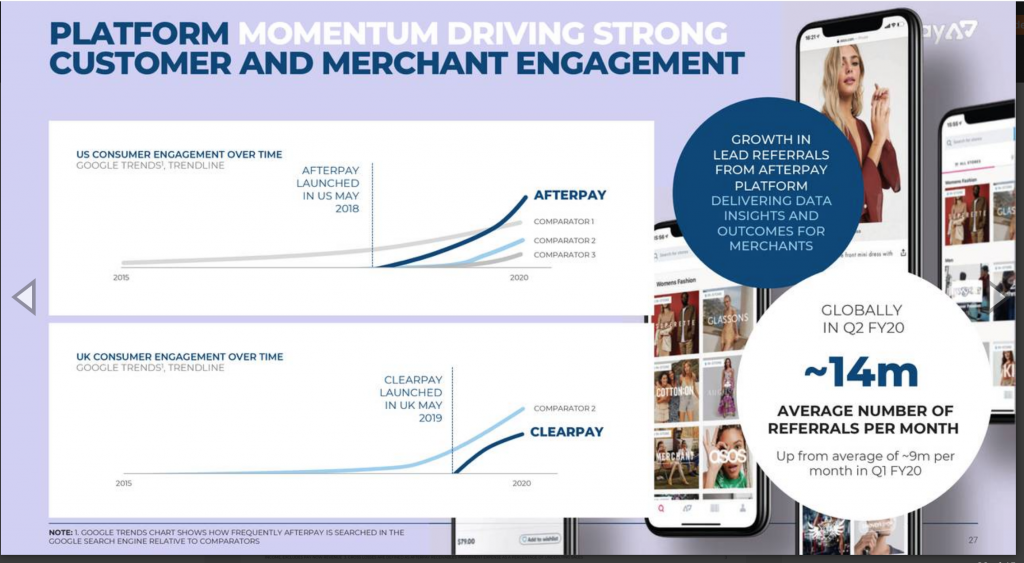

Another standout feature has been ‘shop directory’, or an area listing all stores and shops accepting Afterpay online or in-store. What debuted as a tool has quickly become a fresh business growth driver, Al-Bassam said. “We have become a primary referrer of lead traffic to merchants,” he said. “We didn’t design this capability to make money, but to use this to fulfil core ethic, which is connecting consumers with merchants. And it’s taken off and become an important part of Australian retail e-commerce. We didn’t expect that.” As Fogelberg described it, Afterpay’s mobile app has become a shopping destination in its own right. “The app is a place to start the shopping experience as a consumer,” he explained. “As a consumer, if I’m trying to get across different shops, I can search in-store merchants via maps. It’s become an easy way to find the merchants consumers are looking for. That focus on buying behaviour and the Afterpay website as an entry point has escalated in the two years since the app debuted.” Since then, the directory has evolved to include additional brand and category search functionality. Afterpay has also gone from 1000 merchants to more than 27,000 and counting, stretching across health, retail, services and more.“We now know it’s an area to focus on and you’ll see Afterpay putting more investment into these experiences,” Al-Bassam said.

Another important app innovation has been the ability to track orders. “We had a web portal, but feedback was people wanted this in the app, as they access Afterpay often both for future payments plus making payments,” Al-Bassam added.

From mobile to digital transformation

Work on the app was swiftly followed by a digital project re-architecting and rebuilding Afterpay’s web platform. Thanks to rapid local and international uptake, the site was falling to its knees, unable to cope with loads and traffic spikes, Fogelberg said. Six months in, Dovetail started rebuilding the web portal from scratch. This included a technology infrastructure refresh and new payments process, consumer-facing design and integration with the mobile app via APIs. The key priority with Dovetail was executing very quickly, Al-Bassam said.

The other imperative has been internationalisation. Last May (2018), Afterpay made its debut in the US, gaining more than 1m customers in 11 months. This came off the back of launching in New Zealand two years ago. The company has also set its sights on the UK. Al-Bassam noted the focus includes launching cross-border trade and allowing users to purchase from merchants outside their primary market. “You can’t go through the rapid growth we have in the last three years without significant changes in how we approach things, our culture and so on,” he continued. “Three years ago, we were a much smaller company and 100 pcfocused on Australia. Today, we have offices in Sydney, Melbourne, Auckland, San Francisco, London and Manchester. That reflects a great deal of cultural, execution and process changes, as well as growing the number of people and partners servicing the business to help with geographic breadth.

Balancing resiliency with scalability

From a technical point of view, there’s a constant trade-off between architecture that is scalable, and being able to make digital changes quickly, Frandsen said. “Some large firms have incredibly scalable architecture, but it’s hard to make changes. Afterpay is moving quickly. A key driver in all technology choices here has been managing that trade-off,” he explained. As Frandsen pointed out, some companies build for 20m customers when they have 20,000. While that’s a step too far, you can’t just build for current demand because it means you can’t grow, he said. “You have to decide where on the spectrum you sit: Scale versus building new features and functions.” What’s more, rebuilding back-end and servers had to be done while the site was live, with components swapped out as demand continued to grow and the feature-set became more complex. An exponential spike comes with Afterpay’s biannual key 48-hour sales promotion, AfterYay, which triggers site loads that have never been tested in production. This has required monitoring and dynamic server load scheduling, Fogelberg said. As Afterpay expands globally, compliance, risk mitigation, tailored value and feature sets and platform availability continue to be real challenges. “It’s a balancing act – to launch a website that’s flexible in how that’s done,” Fogelberg said.

Metrics of success

Among measures of success for Al-Bassam are consumers downloading the app, plus positive customer feedback in terms of NPS (net promoter score, a management tool that can be used to gauge the loyalty of a firm’s customer relationships) and app store ratings. Other metrics are engagement and retention and active monthly users. For the Dovetail team, stability and availability, while hygiene factors, are non-negotiable. “Significant downtime has massive impact on Afterpay’s revenues,” Fogelberg pointed out. “In terms of commercial metrics, a key one is growth, both in terms of improving single customer and engagement and retention, as well as growing and saturating the market.” Today, Afterpay represents about 10pc of Australian retail transactions, showing there’s plenty of scope to expand. Other metrics both parties are keeping a watchful eye on are growth in raw customer numbers and monthly users. “You can be good at bringing in customers, but keeping them engaged in the long term is something most digital companies and startups fail at. Afterpay has built loyalty and long-term customers and is keen to keep it that way,”

US expansion proceeds at pace

“In January 2018, US venture capital fund Matrix Partners announced its intention to invest AU$19.4m in Afterpay to support its entry into the US retail market, which was worth US$3.8 trillion in total annual turnover, including US$450bn in online purchases. Afterpay launched in the US in mid-May 2018 with retailers such as Urban Outfitters and over US$11m of underlying sales was processed in the first full month in June 2018. By August 2019, the company revealed that it had over 2m active users and 6,500 merchants in the US and announced a strategic partnership with Visa in the US to help it acquire new merchants by smoothing integration processes. On 21 May, 2020, the company announced that its US operations had grown to five million active customers in the US. Furthermore, it revealed that in total there were nearly nine million U.S. consumers who had joined the platform since its launch two years prior.”

Even faster in the UK.

“In August 2018, Afterpay entered into a share purchase agreement to purchase Clearpay, a UK based buy now pay later subsidiary of Thinksmart. Under the agreement, Afterpay acquired 90pc of the equity in Clearpay for a total consideration of 1m Afterpay shares. Afterpay has the option to purchase the remaining 10pc in any time 5 years subsequent to the purchase. In June 2019, Afterpay announced that it had launched in the UK under the Clearpay brand. In its 2019 financial year update, the company announced that its growth in the UK was faster than that of the US, with more than 200,000 customers in the UK over its first 15 weeks,”

More on the US opportunity

“While instalment loans were not quite unheard of in the U.S. five or six years ago, they were quite rare. At that time, the U.S. market for retail credit was largely occupied by store-branded cards and revolving credit accounts. But as millennials’ and Gen Z consumers’ enthusiasm for store cards has cooled, a host of startups have stepped into the market to offer instalment financing at the point of sale (POS) as an alternative product. But, as Afterpay co-founder and CEO, Anthony Eisen, told Karen Webster in the second half of their “How We Did It” conversation about the company’s U.S. launch, the products that emerged have had some similarities. In general, he noted, they tended to be pitched to big-ticket, once- or twice-in-a-lifetime purchases like appliances, travel, furnishings and the like. And they were very much credit products — more transparent and easily understood than revolving credit store cards but still offering long loan terms and interest fees. There is nothing wrong with that kind of product, Eisen noted, but it is not what Afterpay built for its founding day in Australia, nor what it is hoping to offer. “You’ll never see Afterpay offering loans to people that extend over many years and reflecting things that people want to buy once or twice in a lifetime,” said Eisen. “We’re there for those lifestyle categories and the things that are really important to customers that they don’t want to get into debt around — that’s our purpose.”

What brought Afterpay to the U.S. market two years ago, he noted, was basically an invitation from their merchants — because there was no comparable product already existing there. That didn’t necessarily make the launch smooth sailing — there are the standard regulatory challenges in entering a new market, as well as the necessity of making sure their tech stack was fully loaded and ready to scale into a market that is much larger than Australia in all dimensions. And because their service is novel, there was the need to offer simple and transparent education to both prospective customers and potential business partners.

So far, so good, said Eisen. In fact, that launch into the U.S. has exceeded initial expectations in terms of merchant and customer acquisition — a fact that he largely attributes to starting in the right place in the market and making the right offer at the right time for both sides of their platform. Applying the lessons they learned in Australia, Afterpay began in the beauty and apparel sectors in the U.S. The goal was to build a presence in the areas that are important to customers in terms of their routine purchases — and beauty and wellness, particularly in the U.S., offers a remarkably deep opportunity. The U.S. market in those two areas alone, Eisen noted, is more than four times the size of the entire Australian e-commerce realm.

And that opportunity will expand — in Australia, they are pretty well-diversified across verticals, Eisen pointed out. But the same basic opportunity exists in the U.S. — to both establish a presence and to make a quick and noticeable difference to customers’ (especially millennials’) financial lives. In short, said Eisen, it is an excellent place to enter the market and quickly grow scale with a wide swath of merchants and brands. The big brands are important, of course, but for Afterpay, discovery of small- to medium-sized businesses and mid-market businesses is also a priority — and the Afterpay customer tends to tap the brand for more than just financing their purchases. “We’ve tried to encourage a mix of retailers across our platform,” said Eisen. “If you look at the over 40,000 retailers we have on the platform, we’ve got all the very big brands you’d expect, but also thousands of smaller businesses. The ability for Afterpay to reach customers for those businesses has been a huge advantage to them, because we drive a lot of traffic.”

And that traffic comes ready to shop.

Consumers, Eisen noted, want spending flexibility — they don’t necessarily want credit products, particularly complex ones that require using a specialised calculator to figure out interest. Merchants want to offer up that flexibility, because at the end of the day, it serves two purposes: It brings more customers to the shop and makes them more likely to spend more while they are there. “What we found and continued to deliver was significant incrementality, measured by increased basket sizes and average order value, and also in repeat transactions, as well as in providing for lower returns,” Eisen said. These are all things merchants want, he noted, and Afterpay’s goal in the U.S., Australia and worldwide is to be the bridge between what the merchant and consumers want by taking on the risk and making the interactive path easier. It won’t be easy, Eisen admitted — growth is always challenging, because every market is slightly different, and identifying and pitching to local needs is always a custom build. That said, he believes it is a product worth expanding.”

If you think of Afterpay as disrupting a massive market by replacing the use of expensive credit cards by an interest free alternative I think you get a feel for the scale of their opportunity. What they offer seems very simple but requires sophisticated technology to make it work. Beyond that the shop directory is turning them into a platform on which merchants and their customers can engage. It has the makings of a very large global business.

I have included some slides below to give a graphic flavour of how fast the group is growing and the scale of their opportunity. One key driver is that the longer consumers are on the platform the greater the frequency of their purchases. It is not for nothing that Nick Mornay has described Afterpay as a ‘once in a lifetime opportunity’.

Hyper growth on the scale being demonstrated by Afterpay makes investors nervous. This is understandable, one false step and the shares can tumble. They can even tumble because investors are scared by say an emerging pandemic as we saw in March, when the shares lost some 80pc of their value in little more than a month. I guess investors may have feared that the group was going to be buried in bad debts as customers lost their jobs and potentially defaulted even on their modest liabilities with Afterpay. The fact that didn’t happened has correspondingly raised confidence in the business model. The shares look a phenomenally exciting investment in a business that is growing explosively but could be at an early stage in its growth – a once in a lifetime opportunity indeed.