It’s not hard to be a successful investor, just buy and hold shares in the best companies

| Ambarella | AMBA | $105 |

| Apple | AAPL | $140 |

| Argenxs SE | ARGX | €253 |

| Ashtead | AHT | 3731p |

| Atlassian | TEAM | $225 |

| Beigene | BGNE | $375 |

| HelloFresh | HFG | €72.50 |

| ITM Power | ITM | 672p |

| iShares World Momentum | IWMO | $61.16 |

| Maxcyte | MXCT | 665p |

| Mongo DB | MDB | $365 |

| Monolithic Power Systems | MPWR | $385 |

| Netease | NTES | $124 |

| O’Leary Internet Giants | OGIG | $58.50 |

| PayPal | PYPL | $243 |

| SpringWorks Therapeutics | SWTX | $83 |

| Teladoc Health | TDOC | $275 |

| Turning Point Therapeutics | TPTX | $129.50 |

| Twilio | TWLO | $373 |

I have been an investor for a very long time. I think I was 11 when I bought my first shares back in the days when the TV screen in your living room was the size of the latest iPhone screen. I have noticed that people unfamiliar with the stock market regard it as something deeply mysterious, the realm of so-called expects, a treacherous world beyond the ken of ordinary folk.

Not only is this nonsense but stock market ‘experts’, as with experts in so many fields, need to be treated with great caution, not least because it is so rare to find the experts in agreement and when they are they are invariably wrong. I literally pay zero attention to experts. I know what I know and equally important, I know what I don’t know, like where the market is going tomorrow. I have absolutely no idea.

What you need to succeed as an investor is not expertise, at least not a whole library full of it but common sense. Many investors do two things wrong. First, they try too hard and end up with what one perceptive observer has called ‘analysis paralysis’. There are so many variables out there. If you try to take them all into account your brain overheats and it is hard to decide anything.

Second, they try to achieve the impossible. There is a famous breed of speculator out there called a day trader. In competition not only with thousands, maybe millions of other day traders but with algorithms being crunched by hedge fund managers on their super computers they want to buy at the bottom, sell at the top and do it all in a 24 hour period.

Good luck with that, say I. If you can do it successfully without committing fraud you are very special, so special that I have yet to meet such a person. There is a reason why 75pc of investors on IG lose money and the reason is that they try to be day traders.

I remember explaining once to a would-be subscriber what I did. He listened for a bit and then said that was all very well but he wanted to make money quickly. I told him that in that case I was not his man and my service was not for him. Although, curiously enough, I have noticed that a patient approach to investing can often produce surprisingly rapid returns. The mistake is to set out to achieve quick returns; that almost never works.

I am not a day trader but I do invest on IG. I even use leverage and buy things like bitcoin but I don’t lose money and I don’t try to make money quickly. I invest on IG just as I would if I wasn’t using IG and I wasn’t buying CFDs. They are all shares to me, tiny bits of a company in which I am becoming a part owner and I buy and hold, managing my portfolio in exactly the way I advise my subscribers to do.

Except that for many of them I appreciate that leverage is too stressful and they mostly buy shares rather than CFDs, which you can also do on IG, with ISAs, SIPPs or whatever. I like taking risks and get bored if I don’t so I am very much a foot to the floor kind of investor, which doesn’t always end happily but overall I do well.

I don’t get paid by IG but we have to use some platform to buy and sell shares and I find they work very well. I even appreciate their ruthless approach to margin trading. If you get too deep in the red they sell you out. They don’t do fractional investing, where you can buy a fraction of pricy shares like Amazon so if you want to do that you may need to look around. I don’t need fractional investing because my minimum investment is big enough for high-priced shares.

The art of common sense investing

A share is exactly what it says, a small piece of a business. The difference between you and the CEO is that he usually has more shares. These days he may have many more shares amounting to a sizeable piece of the businesses because so many companies are run by the founders. We no longer think of the CEO or even executives on the so-called C-Suite (top management) as hired hands but fellow owners, who also happen to be running the business. Very often most of their remuneration comes via share stakes and options rather than salaries, which can be surprisingly modest.

If you hang on to that idea of a share (or a CFD or even a spread bet) as being part ownership rather than some mystical financial instrument then it quickly becomes obvious that the thing you want to own is a piece of a good business, ideally a very good business.

I think most investors do realise that but they then confuse the issue with a whole raft of other considerations. Are the shares cheap or dear? Is the whole market cheap or dear? What is going to happen to the economy? What about inflation and interest rates and the election and the roll out of the Covid vaccine and the possibility that Iran or North Korea might have nuclear weapons, which might lead to tensions with the US, which might affect the stock market and so on and so on?

Maybe it is because novice investors think they need to have the answers to all those questions that they find the idea of investing so daunting? The truth is you don’t need those answers (a) because nobody has got them and (b) because even if you did have them there would still be no guarantee that you would take better decisions.

My approach to investing has become very stripped down over the years. I really just want to know one thing. Is this company a great business with exciting growth potential? If it is, I want a piece of it and once I have got that piece I will keep it until it is clear that it is no longer a great business. If it is not a great business with exciting growth potential, I won’t touch it.

Just in case that still seems to leave things complicated I have another simple rule. Not only am I not afraid of the obvious, I positively like obvious. So if rule one is only buy shares in great businesses, rule two is – if it is not obvious that it is a great business, it isn’t; that saves a great deal of exhausting and ultimately fruitless cogitation.

It is a key reason why I am able to identify exciting shares so quickly. I know what I am looking for and long experience and maybe some sort of knack helps here but ultimately, if it is not rapidly apparent from the numbers, the share price behaviour and the things the top management are saying that the business is exciting, I move on.

I miss a few with this approach but I also spot a lot, often early in their climb to great success. Netflix is presently trading around $555. I first recommended them at $8.48 (price adjusted for subsequent share price splits) and at that time CEO, Reed Hastings, was as gung-ho on prospects for the business as he is now.

Among more recent stars I first recommended Shopify at $75.20 in April 2017. They were $35.50, when I first put them on my watch list. The latest price is $1,185. More recently still, I recommended shares in Hong Kong-based stockbroking and wealth management business, Futu Holdings, in July 2020 at $29.40 and five times since and the latest price is over $114.

What these shares and the others featured in Quentinvest have in common is that they are all what I call 3G (great chart, great growth, great story). This may sound complicated but again it boils down to common sense. I don’t spend hours, or even minutes, analysing share price charts. What I am really looking for is a strongly rising share price. If it isn’t going up strongly (a) why bother and (b) I become very suspicious if I think that I am the only person who knows the story because that never happens.

Great growth is also obvious. It doesn’t have to be profits or even sales, though it usually is but some metric important to the performance of the business has to be rising strongly. If nothing is then again, why bother.

Last but not least and arguably least obvious is great story. I have an advantage here because over the years I have studied thousands of companies and interviewed thousands of top executives. It is likely that this has given me a nose for a great story but even so they are usually pretty obvious. If you can talk to the CEO, which I don’t do anymore because it is all available online or read the annual report and you still don’t think the company is exciting, it most likely isn’t.

An even simpler rule is – are the top management excited about the performance and prospects because if they aren’t why should you be. It is not so much that I am a better analyst than you that I find so many great stocks. It is more than it is my day job. I spend more time looking and I know loads of short cuts to help me in my search.

How I use charts

There is considerable debate about whether charts work in the sense of whether looking at past share price action tells you anything about the future trend in share prices. It obviously doesn’t in any absolutely reliable sense or all chartists would be millionaires but I do finds charts useful, even indispensable.

They are my first port of call with a share I have never encountered before because I love to see a strongly rising share price. Any kind of flat-lining kills my interest very quickly.

I also use charts for timing decisions and although my strategy does not depend on selling shares it is unlikely I would hang on to a share if the long term moving averages were both falling. There are too many rising shares to bother with those that have signaled that they are in a bearish (falling) trend.

I don’t bother with complicated technical analysis of the sort practised by some chartists. Again my rule is that if the message is not obvious there is no message. Developments which I treat as buy signals include breakouts above resistance. So if a share hits 90 five times, falls back each time and then blasts through 90 ($, p or whatever) I will be a buyer. If a share stays strong in a weak market I will incline towards buying. If a share is persistently strong I will be a buyer and if the whole market takes a dive I will be ready to buy favoured shares showing signs of recovery or just holding up well.

I do need some sort of positive sign. I never try to catch a falling knife so I never buy into a falling share or a falling market. It has to be clearly on the turn because you never know how bad a fall is going to be. I have seen some big ones in my time,

HelloFresh looks tasty

HelloFresh (HFG) is a good example of a share which is classic 3G. The chart (not shown) is strong. In around 18 months the price has gone from €8.50 to €72.60. (I have alerted them six times starting at €21.10). Some people might feel it is too late to buy. I never think that; if a share is going to climb to the moon it needs to climb sharply so unusual strength is a good sign.

The growth of the business is terrific with sales of €905m for calendar 2017 projected by analysts to reach almost €5bn by 2022.

The story is exciting. HFG delivers meal kits. In itself that is no big deal but they do it at scale. In 2019 they delivered 280m meals, in Q3 2020 they had 5m active customers, their turnover in 2019 was €1.8bn and they have over 7,000 employees.

These guys don’t just deliver meal kits; they are the Usain Bolt of meal kit delivery and that’s important because the same characteristics that have taken them this far are likely to take them a great deal further. The CEO, Dominic Richter (HFG is based in Berlin) is also the founder, which I like. The chief operating officer, Thomas Griesel, is another founder.

They go to a lot of trouble to explain to investors what the business is all about, which is another good sign, not least because it suggests they know what they are doing and how they are doing it. They are moving fast to go global, which is critical to seizing first mover advantage in a large and competitive market place. And they are ambitious as they spelled out on their capital markets day, held on 10 December 2020. Their mid-term ambition is to grow sales to €10bn with double digit profit margins and they note that they are still tiny compared to the market (€13.3 trillion across 14 HFG markets) they serve.

As Jack Nicholson didn’t say to Greg Kinnear in the film ‘As Good as it Gets” – that does it for me.

Ambarella AMBA Buy @ $105

Ambarella’s low-power SoCs [systems on chips] offer high-resolution video compression, advanced image processing, and powerful deep neural network processing to enable intelligent cameras to extract valuable data from high-resolution video streams. The company boomed between 2013 and 2015 supplying kit for devices like video security cameras then went quiet. Sales have been falling between 2017 and 2020 but analysts are projecting strong growth over the next two years. On 11 January 2021 AMBA introduced CV5, saying ““With the introduction of CV5, Ambarella is defining the next generation of automotive, consumer, and robotic cameras.” Sounds exciting! In the latest results CEO and founder, Fermi Wang, said “The megatrends for security, safety, and automation are very favorable, and the pandemic appears to be accelerating this digital transformation. To support this anticipated growth, we continue to build our team globally, and we intend to further expand our presence around the world to support the rising interest in our CV SoCs from both existing and new markets.”

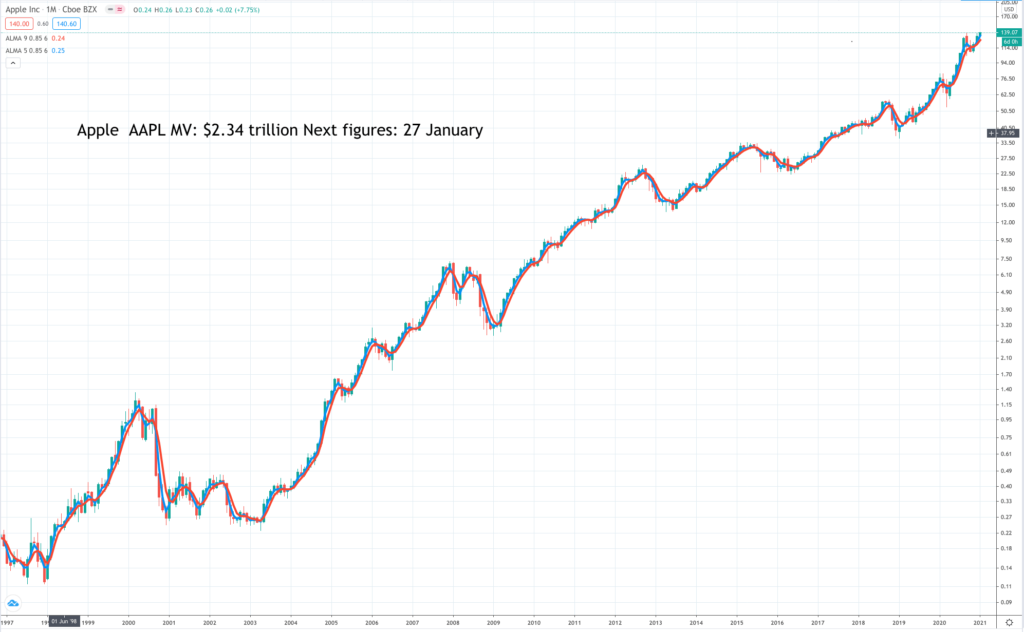

Apple AAPL Buy @ $140

Apple is due to report shortly, which may make the shares volatile. Analysts crunch endless numbers trying to second guess the figures. I am more interested in the big picture. Projections are for steady growth in coming years with net cash swelling to almost $200bn by the year to 30 September 2023. Key drivers in recent years have been the rapid growth in sales of devices like watches and Airpods and the growth of recurring income from the successful services business. Exciting developments on the horizon include 5G smart phones and the Chinese market is important for Apple. In broad terms Apple is the world’s greatest devices business with the number one brand to which it is adding new devices and adding a swelling services business. The strong balance sheet funds growing returns to shareholders and there are wild cards like cars, where Apple is surely planning something. It also has a great leader in Tim Cook.

Argenx SE ARGX Buy @ €252.50

Argenx is one of a number of biopharmas doing well on the stock market and one of four featured in this issue of ‘Great Charts’. The company describes itself “as a global immunology company developing antibody-based medicines for patients suffering from severe autoimmune diseases and cancer”. Argenx is evaluating its lead candidate, efgartigimod, in multiple serious autoimmune indications and cusatuzumab in hematological malignancies. In the latter the company is in partnership with Janssen, while for the former it recently entered a partnership with an exciting Chinese biopharma, Zai Lab, also in the QV portfolio. Sales are expected to rise fivefold in the next two years but the key share price driver will be news flow. This is what they said with the latest results “We are in a very strong position as we close out 2020 and look forward to our first commercial launch next year. We know that FcRn antagonists, as a new class of medicines, have tremendous potential to transform the treatment of serious autoimmune diseases.”

Ashtead AHT Buy @ 3731p

Plant hire group, Ashtead has become one of the wonders of the London stock market. Plant hire businesses own and rent out plant, which is financed by debt. On top of that they bought NationsRent for $1bn in 2006 to dramatically enlarge their US operations. In the 2008 financial crisis many feared the group would collapse and the shares fell to 24p. Then came a miracle. The financial crisis forced many US businesses to look at their balance sheets and triggered a massive shift from owning to renting leading to a massive boom in Ashtead’s Sunbelt Rentals business, which has grown like topsy almost ever since as rental became the norm in construction, at exhibitions, shows and all over the place. The group is the number two player in equipment rental in North America, strong in the UK and stands to benefit from a likely boom in infrastructure spending as we emerge from lockdown.

Atlassian TEAM Buy @ $225

Like Apple, Atlassian is due to report soon and this may trigger volatility. Founded by two Australians, who still run the company, Atlassian released its flagship product, Jira– a project and issue tracker, in 2002. In 2004, it released Confluence, a team collaboration platform that lets users work together on projects, co-create content, and share documents and other media assets. The business sells its software to team managers and developers and has grown from those early beginnings to the point where sales are projected to reach nearly $3bn in the year to 30 June 2023. The business is global with a big chunk of sales in the US. Part of the secret sauce at Atlassian is that the group spends massively on r&d to make the products great value for customers. As a result it doesn’t need to spend so heavily on sales and marketing. In its latest financial year the group generated free cash flow of $500m and spent an incredible $768m on r&d. The group said recently it sees sales going to $5bn and beyond.

Beigene BGNE Buy @ $375

Beigene is a Chinese-based biopharma targeting the Chinese market but founded and led by an American, John Oyler. He founded BioGene in 2010. This is what he said about why. ““When I started considering how reimbursement was shifting from less evidence-based medicine to the latest and best medicines in the world, I saw the incredible opportunity China held for our industry. The country had the capability to pour tens of billions of dollars back into the global industry to help pay for more research, which would not only make drugs more affordable in China, but across the globe. That could be transformative for patients and the industry. So, to me, it seemed like an incredible opportunity and time to build a company that could play a role in that, especially if focused on oncology.” BioGene is doing all of those things, developing its own drugs and building key partnerships with biopharmas in the US and the rest of the world. It is an exciting time and the company is announcing developments at breakneck speed.

ITM Power ITM Buy @ 672p

ITM Power, a sustainable energy business focused on hydrogen, has practically doubled in valued since being featured in last month’s issue of Great Charts. We will learn more when the company reports on 28 January but meanwhile there are some important things happening and of course we now have leaders in the UK and US, who are positively competing to show how green they are. News from the company is coming thick and fast including a deal to sell to German chemical giant, Lindt, a 24MW [megawatt] electrolyser to be installed at the Leuna chemical complex in Germany. This new 24 megawatt electrolyser will produce green hydrogen to supply Linde’s industrial customers through the company’s existing pipeline network. In addition, Linde will distribute liquefied green hydrogen to refueling stations and other industrial customers in the region. The total green hydrogen being produced can fuel approximately six hundred fuel cell buses driving 40m kilometers and saving up to 40,000 tons of carbon dioxide tailpipe emissions per year.

iShares MSCI World Momentum IWMO Buy @ $61.16

Although priced in US$, IWMO is an ETF listed in London. I couldn’t show the whole chart, which reveals a sustained uptrend since launch in October 2014, because of a mistake on the chart but it is still apparent the shares are doing well. They are well on the way to trebling since 2014, which is not as good as the Nasdaq 100 but not too far behind. The fund is focused on global shares in strong uptrends. It has 350 holdings of which the top 10 are all the usual suspects led by Tesla and Apple. The top 10 holdings account for 36.21pc of the portfolio and every single one is in the QV for Shares portfolio. In strict performance terms QQQ, an ETF, which tracks the Nasdaq 100, has done better but is not UCITS, whereas IWMO can be bought to go into your ISA, SIPP or whatever.

Maxcyte MXCT Buy @ 665p

US-based but Aim-quoted, MaxCyte, is a clinical-stage global cell-based therapies and life sciences company. As the inventors of the premier cell-engineering enabling technology, the company helps bring the promise of next-generation cell and gene-editing therapies to life. They say 20 of the top 25 and all the top 10 pharma are clients. The numbers are strong but small. Revenue is forecast to grow from $14.0m for 2017 to $38.9m in 2023 with a big leap in the latter year. The company is hiring at a senior level, entering partnerships and raising its profile via attendance at investor events. 2020 revenues are expected to be $26.2m, up 21pc v last year and ahead of market expectations for FY 2020. This growth reflects the increasing adoption of the company’s products and technologies and was buoyed by the launch of an expanded ExPERT™ range of disposables in 2020, which broadens applications available to customers

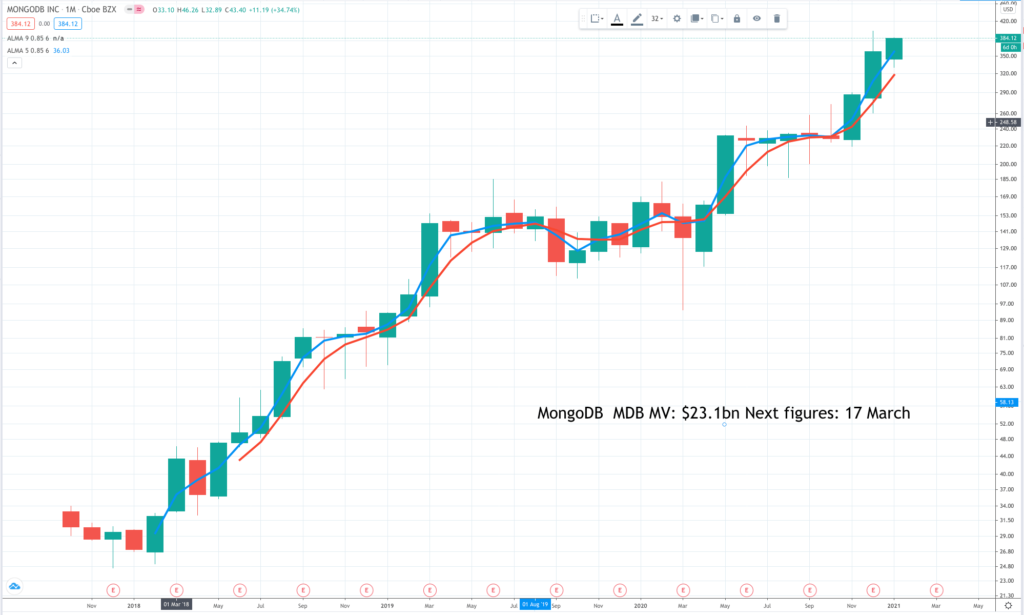

MongoDB MDB Buy @ $365

MongoDB is another enterprise software company, which sells its products to developers. One estimate suggests there are around 27m developers globally and that software is the driving force of the world – with an estimated 9 trillion devices in use, it is the glue that connects people from across the planet. Software developers are shaping and building the modern technological world. Another key driver is data and MongoDB has developed a new approach to managing data in data bases that developers love. MongoDB CEO, Dev Ittycheria, says “we’ve built a database that’s incredibly easy to use, that is applicable for almost every conceivable use case, and is engineered for mission-critical workloads.” Business is booming. In Q3 2020 revenue rose 38pc and within that the self-serve division, Atlas, grew by 61pc to 47pc of total revenue. He concludes – “We are executing at a high level, acquiring new customers at a record pace and deepening relationship with existing customers by building on our core competitive strengths of technical superiority, developer mindshare, and platform independence.”

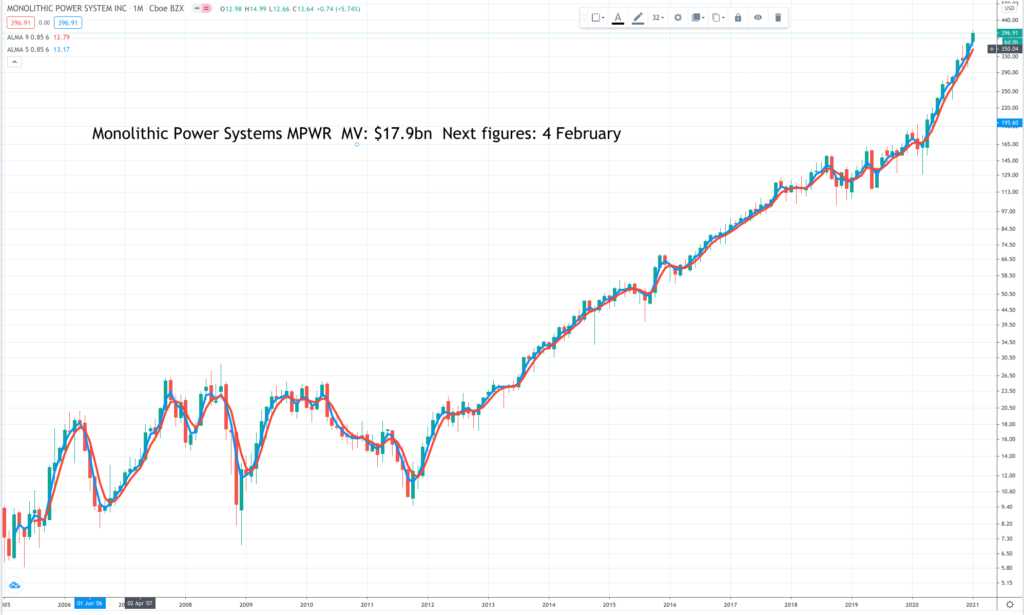

Monolithic Power System MPWR Buy @ $385

Formed in 1997, MPWR says the company has three core strengths; deep system-level and applications knowledge, strong analog design expertise, and an innovative proprietary process technology. These enable MPWR to deliver highly integrated monolithic products that offer energy efficient, cost-effective solutions. Sales are projected to grow from $471m for 2019 to $1099m for 2022 with eps rising from $1.50 to $4.88. Latest sales grew 59.7pc over a year earlier as capacity constraints eased and some Chinese customers pulled sales forward because of trade issues. The group says “We believe MPWR’ s market share will continue to expand in the coming years as we have been awarded multiple design wins in infotainment, smart lighting, ADAS and autonomous driving”. When asked what’s next after the company reached a $1bn revenue run rate for the first time, CEO, Michael Hsing, said “We’re shooting for $2 billion.” I’m still relatively new to MPWR, a semiconductor business, but the more I learn the more excited I become.

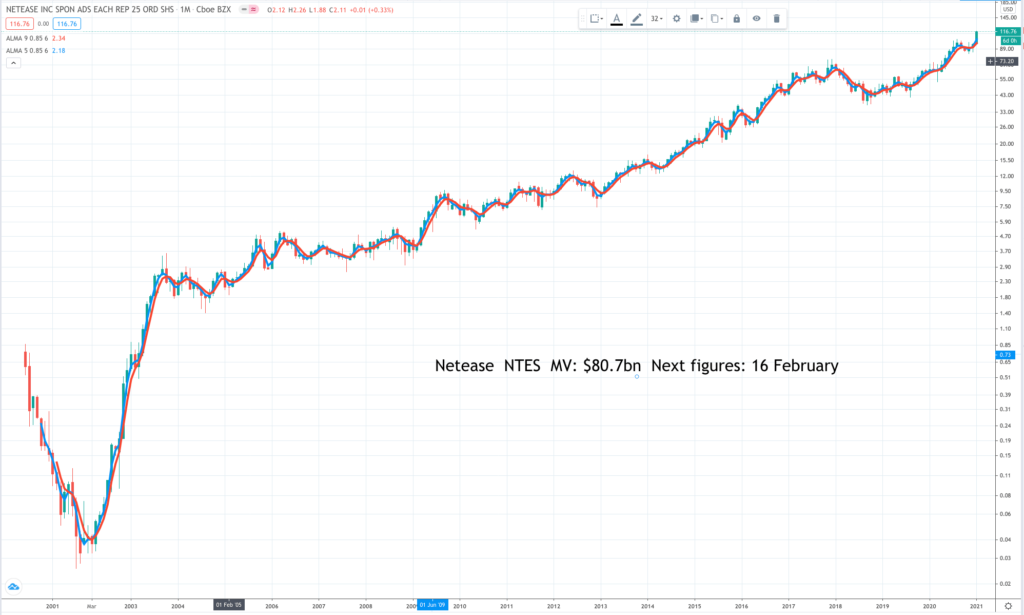

Netease NTES Buy @ $124

Netease is best known as a Chinese video games business that ranks second after Tencent by market share in the Chinese market. The video games business is growing but not at the rates being achieved by other fast growing businesses in the Chinese technology/ consumer space. Many years ago I came across a management consulting presentation which divided businesses into cash cows and growth stars. Video gaming is the cash cow business for Netease and doing well enough to drive expected free cash flow for 2020 of CNY16.4bn for 2020, which is around US$2.5bn but there is also an impressive growth star in the online education business, Youdao. This is a mixture of online courses and learning devices and in the latest quarter sales grew by 159pc to CNY896m (US$139m). Other Netease ventures include online music and an ecommerce label, Yanxuan.

O’Shares Global Internet Giants OGIG Buy @ $58.50

OGIG is an amazing ETF. Since the March low point, hit as markets realised what a threat Covid-19 posed, shares in OGIG have roughly trebled. Most ETFs passively track an index but OGIG is a bit different. The fund does track an index, but one, which is managed according to a set of rules, which has the effecting of focusing the fund on many of the stock market’s most exciting shares. As a result its portfolio has much in common with the QV for Shares portfolio, which is also performing very strongly. I have just had a look and the top 15 OGIG holdings are all in the QV for Shares portfolio. They should hire me or I should stop working and copy them. In total there are 72 holdings with the top 15 accounting for 44.6pc of the fund. Unlike IWMO, OGIG has considerably outperformed QQQ, the Nasdaq 100 tracker, since the March 2020 low point.

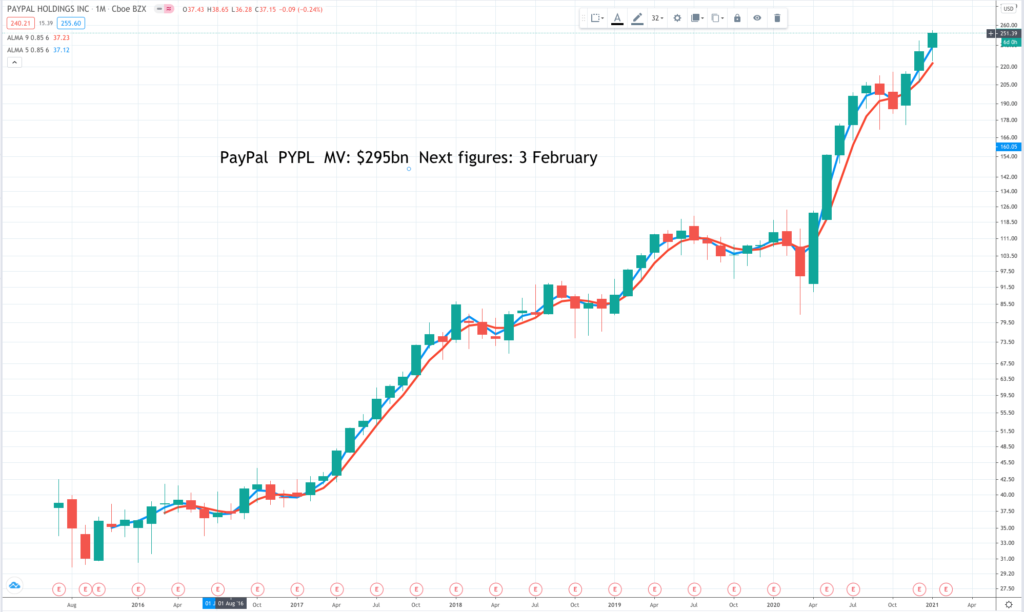

PayPal PYPL Buy @ $243

PayPal is the online payments giant, co-founded by Elon Musk among others, which was bought by Ebay and then demerged onto the stock market. PayPal is now valued at around seven times Ebay so, if you add them both together, Ebay, pre-the spin-off in 2015, has been a phenomenal investment. According to CEO, Dan Schulman, PayPal is an an important inflection point in its history. As he put it “We are investing to create one of the most compelling and expansive digital wallets in the world and you can see this beginning to play out in our strong Q3 results. In Q3, our total payment volume grew by a record 36pc on an FX-neutral basis to $247bn, an annual run rate just shy of $1 trillion. Even more impressive is the growth of our volumes, excluding eBay, which grew 38pc, eclipsing any previous record. We are at a moment in our history where all of our past efforts, our scale, brand reputation, and regulatory relationships position us to play an expansive role in our customers’ lives.”

SpringWorks Therapeutics SWTX Buy @ $83

SpringWorks Therapeutics is a clinical-stage biopharmaceutical company applying a precision medicine approach to acquiring, developing and commercializing life-changing medicines for underserved patient populations suffering from devastating rare diseases and cancer. It sounds like others in the sector but SpringWorks’ strategic approach and operational excellence in clinical development have enabled it to rapidly advance its two lead product candidates into late-stage clinical trials, while simultaneously entering into multiple shared-value partnerships with industry leaders to expand its portfolio. Ultimately, it is successful drugs that will drive the share price making investing a bit of a lottery. I don’t pretend to understand the drugs but I can see that SpringWorks has an impressive leadership team and plenty going on. One of SpringWorks’ key partnerships is with BeiGene.

Teladoc Health TDOC Buy @ $275

Alongside the work from home economy, we are doing many other things from home including engaging with medical professionals. After a strong run as lockdowns gave a dramatic boost to the business the shares have marked time as they absorbed the acquisition of Livongo Health. The deal cost $18.5bn paid for in shares and cash (0.592 TDOC shares + $11.35 for each Livongo Health share). The merger brings Teledoc’s specialty in virtual healthcare together with Livongo’s expertise in the management of chronic conditions. Livongo founder and executive chairman ,Glen Tullman, said the combined company will accelerate the growth of both companies, which already have more than $1.3bn in annual revenues. Latest results from Teladoc Health, which do not include any contribution from Livongo show record revenue of $289m in the third quarter, an increase of 109pc from the prior-year period, including organic revenue growth of approximately 90pc.

Turning Point Therapeutics TPTX Buy @ $129.50

TPTX is the sixth healthcare business featured in this issue of Great Charts giving credence to the idea that the whole sector is on the move. What is certainly true is that a great deal of money is pouring into the sector to fund research into ever growing pipelines. Companies and patients will be hoping this huge r&d spend is going to drive exciting results. What is also interesting is how fledgling biopharmas are coming together to operate in tandem. TPTX recently announced a complex partnership, almost amounting to a sharing of their research pipelines, with Zai Lab, a fast-growing Chinese biopharma. This makes sense because China offers a huge market opportunity, which is impossible to access without a strong Chinese partner, while the Chinese companies want as many drugs in their portfolios as they can acquire. The company’s lead program, repotrectinib, is a next-generation kinase inhibitor targeting genetic drivers of non-small cell lung cancer and advanced solid tumors and is part of the collaboration with Zai.

Twilio TWLO Buy @ $373

Twlio is another enterprise software business, whose products are targeted at the developer community. It is an amazing business. “Our success is a testament to the value proposition that Twilio’s platform offers businesses: digital engagement, software agility and cloud scale. Our goal is to build the world’s leading customer engagement platform.” Talk is cheap but for Twilio this really looks like something, which could happen. Sales are on track to climb from $399m for calendar 2017 to a projected (by analysts) $2,845m by 2022. By then free cash flow should be positive albeit the company will still be racking up losses as it invests at scale in a massive global land grab. Twilio supplements growth by a series of significant acquisitions of which the latest, just announced, is to acquire Segment, described as the leading customer data platform, for $3.2bn in stock. “Together, Twilio and Segment have an incredible opportunity to build the customer engagement platform of the future,” said Peter Reinhardt, Segment’s co-founder and CEO.