Nvidia – the Most Incredible Company in the History of the Planet

February 26, 2024

I am becoming a little repetitive with Quentinvest but I want to hammer the message home. This chart, of the Philadelphia Semiconductor index, looks fantastic. It also looks strikingly similar to the chart of Nvidia (see below). Something amazing is happening to the semiconductor industry. AI is part of that, triggering what seems to be almost infinite demand, especially for the GPUs, software and the whole ecosystem that Nvidia dominates.

Table of Contents

This brings me to a question. Nvidia is probably the most recommended stock in the history of Quentinvest. My question is – do I have any subscribers who do not hold Nvidia shares? My second question to anyone who doesn’t is what on earth are you waiting for and which stock do you hold that you consider a more exciting investment? Answers in an email, please.

Nvidia is the King of AI

I found this on Seeking Alpha.

NVIDIA Corporation (NASDAQ:NVDA) remains the “King of AI.” The company’s most recent earnings announcement demonstrates its dominant presence in the artificial intelligence, or AI, industry. Moreover, Nvidia’s stellar guidance shows that robust growth should continue, suggesting we’re still in the early stages of the AI ballgame.

As far as its valuation, Nvidia remains cheap relative to its enormous potential in the data centre segment and other areas of AI. Furthermore, Nvidia remains the dominant force in the GPU industry, serving as the primary “picks and shovels” company at the base of AI. Therefore, Nvidia’s stock has tremendous potential and should continue moving higher in the long term.

Some estimates are for more than $200bn in revenues next year. Moreover, we will likely see considerably higher sales revisions with yesterday’s blockbuster results. Next year’s average annual sales estimate could be closer to $150bn soon, and the company may report even stronger revenues. Therefore, provided the sales growth potential and Nvidia’s 10-15 times forward sales ratio, its share price appears relatively inexpensive relative to its long-term growth and profitability prospects.

Seeking Alpha, 22 February 2024 (Victor Dergunov, The Financial Prophet)

Depending on what happens the shares could be amazingly cheap.

For fiscal 2025 (next four quarters), the consensus EPS estimate is just around $21.50. However, given Nvidia’s stellar guidance and past beat rate, it will likely report a much higher EPS. A similar 18pc beat rate equates to around $25.38. Yet, higher-end estimates go up to $30. I believe $26-27 in EPS this year is a fair estimate and attainable.

EPS for next year (fiscal 2026) seems extremely low. The consensus figure is only about $27. Higher-end estimates go up to almost $45. My base case fiscal 2026 EPS estimate range is $32-38, so we can use the $35 mid-point estimate to generate a rough valuation for Nvidia now.

With Nvidia’s stock trading around $700 (higher now), it is only about 20 times forward earnings estimates, which is cheap for a company in Nvidia’s dominant market-leading position with remarkable growth prospects ahead. Therefore, despite the recent run-up, Nvidia’s stock likely has much more upside in the coming years.

Seeking Alpha, 22 February 2024 (Victor Dergunov, The Financial Prophet)

Now read what another Seeking Alpha contributor had to say.

When discussing Nvidia, it’s imperative to recognise that GPUs encompass more than just hardware; they represent an entire computing acceleration ecosystem. Nvidia transcends being solely a hardware company, evolving into a comprehensive ecosystem where hardware seamlessly integrates with software, libraries, and applications. This integrated approach offers a substantial competitive advantage, as companies entering such sophisticated ecosystems face soaring switching costs. To grasp the magnitude of these switching costs, consider the challenge of transitioning from your iPhone to any Android smartphone after investing just a couple of thousand dollars in the phone, watch, AirPods, and subscriptions like iCloud and Apple Music. Now, magnify that difficulty to the realm of IT ecosystems, where companies have invested millions, if not hundreds of millions, to enhance their computing capabilities. This substantial investment underscores Nvidia’s wide moat, positioning it to maintain its dominant stance in the accelerated computing niche.

KM Capital, 7 February 2024

One of the many things I like about Nvidia as an investment is that the shares are becoming increasingly impossible to value. Analysts go through the motions and remind us of the risks but how do you value a company which is THE beating heart of the most exciting revolution in human history led by a guy who must surely rank as one of the greatest entrepreneurial visionaries of all time?

All this stuff about PE ratios, free cash flow multiples and market value to sales ratios seems like medieval theorists speculating on how many angels could dance on the head of a pin. This business is priceless. Where would humanity be without it?

A more relevant question is why hold any other share?

I have just been watching an interview with Jensen Huang, CEO and co-founder of Nvidia, where he was talking about the longer-term future of AI and Nvidia. I didn’t understand much of it because Jensen Huang is a geek and talks way above my head.

I had one impression though which is that Nvidia has become so ubiquitous in the world of AI that everybody with any plans in this field will have to engage with them. So, if AI becomes huge over the next decade Nvidia is going to become huge too, whatever huge means – much bigger than it is now.

It’s curious because most people will not have heard of Nvidia which is a business-to-business operation. Many gamers will know it but Joe Public has mostly never heard of the company. It is extraordinary to think that by the end of this year the largest company by market value in human history, if that happens, could be one of which most people have never heard.

This may be something Nvidia will want to change as their hardware and software become ever more present in our lives and as shareholders want the company to achieve a valuation appropriate to its importance, its growth and its profitability.

Jim Cramer Loves Nvidia

CNBC commentator, Jim Cramer, who briefly poleaxed ARM Holdings the other day with some negative comments on its valuation, had this to say about Nvidia.

Ahead of the Big Tech company’s quarterly report, which it will release after Wednesday’s close, Cramer reminded investors why he feels so strongly they should buy, not trade, Nvidia stock.

“Hey, maybe I’m still a believer, but I do know why,” Cramer said. “Nvidia deserves its valuation, and if they take a whack at it tomorrow, when they report—remember, Friday’s another day.”

Cramer conceded that some on Wall Street may be suspicious of the fast and furious growth of Nvidia’s market capitalisation, but said he thinks this success is warranted and poised to continue. He likened Nvidia CEO Jensen Huang to popstar Taylor Swift, saying their success is unparalleled in their respective fields.

“They share kinetic energy and brilliance, and neither’s anywhere near their pinnacle,” he said. “When it comes to artificial intelligence, we could be so early that Nvidia’s equivalent of the ‘Eras Tour’ might still be years away, with a string of hits that’s the envy of the industry.”

Investors shouldn’t overlook Nvidia’s importance in the artificial intelligence space, Cramer added. He suggested many new AI products are all “spawn of Nvidia,” and that as revolutionary as Nvidia software is now, the company probably has more advanced technology in the pipeline.

“Open your eyes, people,” Cramer said. “If you think that Nvidia’s quarter is one and done, you’re also thinking that AI is one and done.”

Jim Cramer, CNBC, 20 February 2024

Unlike with ARM, this time I agree with him.

Earnings Expectations Rise Faster Than the Share Price

What is hard for investors to grasp about Nvidia is the sheer pace of growth. It is so incredible they wonder if it can continue. Fair enough but consider this – what if it can?

A chart [not shown because I could not find it], from Sonu Varghese, global macro strategist at the Carson Group, helps put things in perspective.

It shows how Nvidia’s (NVDA) earnings – or, to be more precise, analyst expectations of its earnings in 12 months’ time – have soared well beyond its stock price, leading actually to a 102-point multiple contraction over the last two-plus years.

That’s not to say Nvidia is necessarily cheap, Varghese said in a message on the social media service X.

“There’s a runway here. Of course, how long can they can keep printing profits like this … that’s the question,” he said. “There’s operating leverage too, with profits rising while sales grow. So margins increasing.”

As MarketWatch’s Therese Poletti points out, Nvidia’s margins in the chip space are only surpassed by ARM Holdings (ARM), the microchip designer.

Nvidia stock surged 16pc to $785.38 on Thursday after the microchip maker beat revenue expectations for the fourth quarter by about $2bn, and also projected first-quarter sales that at the midpoint are nearly $2bn higher.

Nvidia is now ahead of both Amazon.com (AMZN) and Alphabet (GOOGL) by market cap.

Over the last 52 weeks, Nvidia’s stock has climbed 237.2pc

Morningstar, 25 February 2024

Nvidia Now is Like IBM in the 1960s and 1970s

Below is a comparison of Nvidia in 2024 with IBM in the 1960s and early 1970s when that company had a similar domination of the computer space. In terms of AI infrastructure Nvidia’s current domination is even greater at around 85pc.

NVIDIA’s earnings highlight a large, but still early, shift in demand for AI chips and hardware that simply can’t be met by current supply. From a microeconomic perspective that means strong profits from current suppliers, of which NVIDIA is currently the most important. We see that all over NVIDIA’s earnings numbers. Other players will surely be drawn by those profits (it’s already happening) and over time NVIDIA’s advantage will erode, but NVIDIA has a nice lead that should persist for some time.

Remember IBM, a still formidable company but not included among the “Magnificent Seven” of tech-oriented giants, manufactured 70pc of the world’s computers in the 1960s and had become the largest company by market cap by 1966, holding onto the position until the late 1970s. While “Big Blue” may not be a dominant player in hardware anymore, it helped lay the foundation for the continued leaps in computing we’re talking about today. And its more-than-a-decade reign as the world’s largest tech company is impressive. Similarly, while today’s story is NVIDIA, the enduring story is AI. It’s hard to gauge whether to measure NVIDIA’s lead in years (as seems to be the emerging case with Tesla’s lead in electric cars) or the more than a decade that IBM had. But whatever the lead, any ground made up on NVIDIA will likely be accompanied by a rising tide that lifts all ships as the AI space continues to expand.

Carson, 23 February 2024

Below is another intriguing quote from Carson on Nvidia’s latest earnings and AI generally.

“Forget self-driving cars, AI is transforming every industry, and Nvidia is at the center of it all” – Venture Capitalist, TechCrunch

With bated breath, investors eagerly awaited the final earnings report of the “magnificent 7.” Among the seven, Nvidia’s report was perhaps the most hotly anticipated, given it’s the driving force behind accelerated computing and artificial intelligence. This tech darling, responsible for significant market gains over the past year and a half, carried the weight of the entire AI industry on its shoulders. An earnings beat was expected, though how large of a beat left investors wringing their hands. In the days leading up to the report, shares of Nvidia had fallen about 8pc as investors took profits. It turns out, Nvidia beat fourth quarter earnings estimates by $0.57 (~12pc) and raised guidance for the first quarter above expectations. Ultimately, shares climbed back to the level they were at before the nervous excitement began as AI chip demand continued to accelerate.

Generative AI has reached a tipping point and demand for artificial intelligence is exploding. In the fourth quarter, the company’s sales more than tripled and earnings increased nearly six-fold. Demand is extremely robust, and the company will be short supplied for the foreseeable future. Investors expect its earnings will double again in the upcoming year, as Nvidia extends its streak of shattering expectations. CEO Jensen Huang said, “Demand is surging worldwide across companies, industries, and nations.” Nvidia H100 accelerator chips serve as the backbone of artificial intelligence and companies like Amazon, Meta, Microsoft, and Alphabet are scrambling to acquire them.

Generative AI represents a technological leap that pushes past the boundaries of prior generations of computing. Until this breakthrough, computers relied on complex algorithms to crunch numbers, solve equations, and manipulate statistics at ever increasing speeds. Generative AI, however, has the ability to learn, adapt, and create, using not only calculations but also text, images, sounds, and other inputs. This is having a significant impact on various fields, from drug discovery to artistic creativity. Nvidia’s chips happen to be perfect for building and training artificial intelligence models because they are so adaptable. The company developed a software ecosystem over the past decade that makes it easy for developers to manipulate and optimise their chips, as opposed to competitor’s chips that are purpose built and less malleable. Nvidia is clearly in the dominant position for the initial wave of AI, though competitors like AMD and Intel are trying to catch up.

Carson 22 February 2024

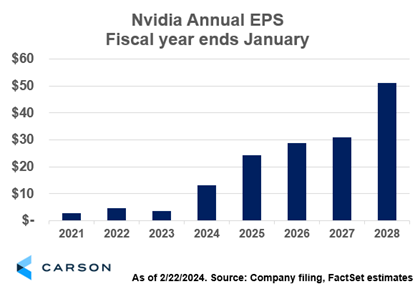

In the fiscal year to 31 January 2023, Nvidia’s earnings per share were $1.74, which was down on $3.85 the year before. Anticipation of this sharp drop in earnings drove the Nvidia share price down to almost $100 from an earlier peak in 2021 around $350. Since then the share price has increased some eightfold but expectations for earnings have exploded. In the chart above expected earnings for the year to 31 January 2028, which is not so far away, are $50, an increase of over 28 times from the 2023 figure.

Even more amazing is that on plausible assumptions the $50 earnings figure could be well exceeded and come sooner than anticipated. One of the quotes above talks about Nvidia revenues reaching $200bn next year (to 31 January 2026); that would be an incredible leap and would take earnings per share close to $50 well ahead of schedule.

How Nvidia Earnings Could Reach $100 Per Share

My finger in the air guess is that given the explosive revenue growth and spectacular profit margins Nvidia’s earnings could reach $100 a share in the current decade. Cramer is no fool and as he says this whole AI/ Nvidia boom is just getting started. We are in an unstable situation where anything could happen and huge opportunities are being presented to companies like Nvidia which are in the right place at the right time.

A wild card not yet discussed is that Nvidia is all about intellectual property and does not have a high capital expenditure budget. It leaves that to its suppliers. This means that as sales and profits rocket higher it will generate dramatic increases in free cash flow which could be spent on an ambitious share repurchase programme, just such a programme as has done so much for the Apple share price in recent years.

Investors are also already speculating on when the next share price split is coming to make the shares more affordable to retail investors.

Strategy – Be Bold, Buy Nvidia, Don’t Be Afraid of Some Leverage

The lesson is to go for it but don’t go crazy like me because that can have unintended consequences like being sold out of shareholdings you have no desire to sell. Two, maybe three times leverage is the way to go and even that should be mostly with profits, not hard-earned cash. Also, don’t be afraid to use spread bets to keep your profits out of reach of the tax man. If you want to buy 100 shares just change the betting currency to US$ and place a 1.0 point daily funded bet which runs forever. Or do the same thing with a long-term spread bet which rolls over at the end of the period. Spread bets may sound scary but it is just another way of buying shares.

Note that you can also transfer your Nvidia shares from wherever they are to a spread betting account. Sell the shares and simultaneously, or shortly thereafter, place an equivalent spread bet.

This is a long-term chart based on 12m candlesticks. It highlights the massive breakout in 2015 and two subsequent breakouts, the latest in 2023. Because it is so long term it has little to say about short-term fluctuations in the share price which can be large but most likely short-lived.

Since the moving averages turned higher in 2013 they have kept on rising. This is consistent with Nvidia’s emergence, in the words of director, Mark Stevens, as ‘the most important computer company in the world’.

It has attained this position both because of its importance in creating the infrastructure for artificial intelligence (AI) and because, in the opinion of many observers, we are still just at the dawn of the age of AI. It is hard to imagine a more exciting situation for a company and its shareholders.

P.S. Several subscribers have emailed me pointing out that they are unable to buy some of the ETFs I recommend because of the KID rules. I will address this problem in a future alert and offer my version of a solution.

Share Recommendations

Nvidia NVDA Buy @ $788

Deep Learning Training v Inferencing

I have just discovered a new dimension to AI which is the difference between training and inferencing. The graphic below sums up the difference.

As I understand it you train your computing system with data on, for example, many different dog breeds so that the computer can distinguish dogs from other animals based on this data even though dogs can be very different from each other. The inference part comes when the computer encounters a dog which is different from any of the dogs on which it has been trained but is still recognisably a dog, not a cat. Sounds easy (it is a skill humans take for granted) but it is not; it takes huge amounts of data and huge amounts of computing power, especially the training part.

The suggestion is that Nvidia is dominant in the training part where computing power is all important but that the inference part may be more competitive as it should involve less powerful semiconductors. We shall see but obviously, Nvidia intends to be a player in both parts.

Here is what we learned from the latest results about Nvidia’s ability to compete in the inference market.

Nvidia built itself into a $2 trillion company by supplying the chips essential for the incredibly complicated work of training artificial-intelligence models. As the industry rapidly evolves, the bigger opportunity will be selling chips that make those models run after they are trained, churning out text and images for the fast-growing population of companies and people actually using generative AI tools.

Right now, that shift is adding to Nvidia’s blockbuster sales. Chief Financial Officer, Colette Kress, said this past week that more than 40pc of Nvidia’s data centre business in the past year — when revenue exceeded $47bn — was for deployment of AI systems and not training. That percentage was the first significant indication that the shift is under way.

Kress’s comments allayed some concerns that the shift toward chips for deploying AI systems — those that do what is called “inference” work — threatens Nvidia’s position because that work can be done with less-powerful and less-expensive chips than those that have made Nvidia the leader of the AI boom.

“There is a perception that Nvidia’s share will be lower in inferencing vs. training,” Ben Reitzes, an analyst at Melius Research, said in a note to clients. “This revelation helps shed light on its ability to benefit from the coming inferencing explosion.”

Dow Jones Newswires, 25 February 2024

Investors are going to worry endlessly that Nvidia is going to be dethroned from its position as the king of AI. This is where you need to have faith. They will fight to maintain their leadership and they have an excellent shot at being successful. The hard bit was getting to where they were, not staying there.